For years, the biggest battle in portfolio construction has been passive vs. active management. That fight has largely tilted in favor of passive strategies, with index funds and traditional ETFs dominating flows due to their low costs and consistent performance. Passive has become the preferred way for many investors to build their portfolios.

However, that seems to be changing. The growth of active ETFs has shifted the narrative.

Active ETFs may be improving the odds of success for active managers. Historically, active management has struggled to outperform benchmarks, especially after fees and taxes. The ETF structure is changing that equation by offering structural advantages that address key reasons active funds have historically underperformed—a potential game changer for portfolio construction.

Active Has Historically Underperformed

For many years, the answer has been clear: index or go home.

Decades of research show that a large percentage of active managers fail to outperform their benchmarks over time. In many categories, fewer than half of active funds beat passive alternatives in a given year, and long-term success rates are even lower. Over longer horizons, only a small fraction of funds both survive and outperform over a decade.

Analysts point to several structural reasons for this underperformance of active strategies.

Fees have been a major hurdle. Active mutual funds typically charge higher expense ratios than passive funds, creating a performance drag that is difficult to overcome consistently. Tax inefficiency has also historically weighed on returns.

Market efficiency—especially in large-cap equities—has made it harder for active managers to consistently identify mispriced securities. Combined with fees and taxes, these challenges have made sustained outperformance difficult.

The ETF revolution only reinforced these facts. Low-cost index ETFs allowed investors to capture better-than-active returns at lower cost.

With that, passive funds have become the de facto way investors gain market exposure.

Active ETFs Are Doing Better

However, investors may want to rethink the passive/active debate. Active ETFs have come to play.

That is the gist of Morningstar’s latest Active/Passive Barometer, which found that the ETF structure has improved success rates for active managers.

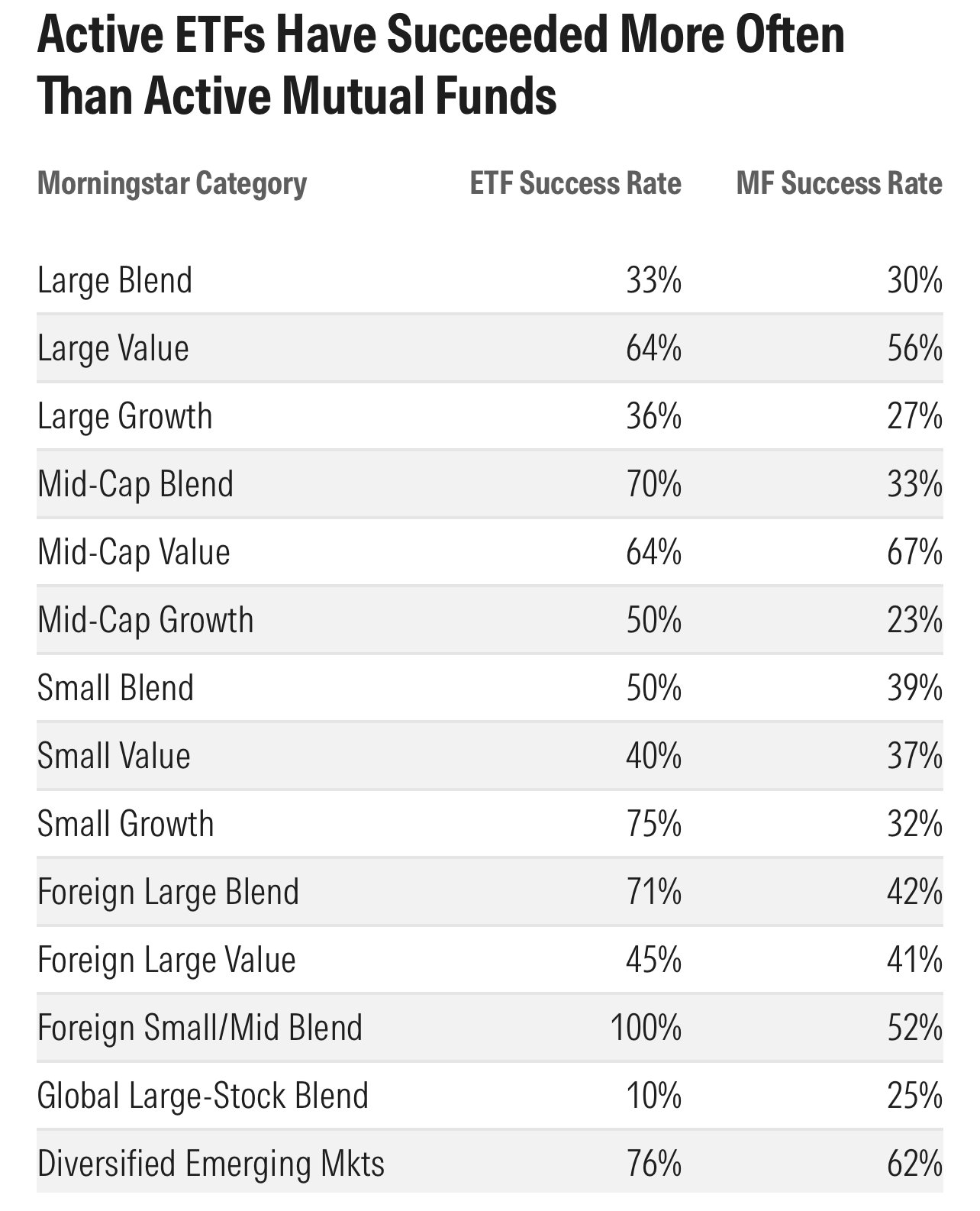

According to the data, active ETF managers have succeeded more often than their active mutual fund counterparts. Looking at three-year success rates, Morningstar found that 50% of active ETF managers beat their benchmarks, compared to just 41% for active mutual funds. ETF success rates were also higher than those of active mutual funds in 14 of 19 categories. 1

This table from the researcher highlights their findings.

Source: Morningstar

Returns were another bright spot. Active ETFs averaged higher returns than mutual funds in 12 of 19 categories, suggesting that active ETF managers are simply performing better than their active mutual fund counterparts.

According to Morningstar, the reasons come down to the ETF structure. While active ETFs are not immune to the challenges of active management, they are structurally better positioned to overcome them.

One of the most important advantages is cost. Active ETFs generally carry lower expense ratios than comparable mutual funds, reducing the performance hurdle managers must clear. Morningstar research highlights that much of the advantage active ETFs hold over mutual funds stems from this lower fee structure.

Tax efficiency is another major differentiator. The ETF structure allows for in-kind creation and redemption of shares, which minimizes taxable capital gains distributions. Described as “irrefutable” in research on active ETFs, this advantage can significantly improve after-tax returns for investors.

Morningstar also highlights liquidity and flexibility as playing a major role in active ETF success. Because ETFs trade intraday, managers operate in a structure that better aligns with market dynamics. The ability to use custom creation and redemption baskets—introduced through regulatory changes—gives managers greater control over portfolio management and trading decisions.

Another factor is so-called patient capital. Unlike mutual funds, which can experience large end-of-day flows, ETFs allow investors to trade shares on the secondary market without forcing the manager to buy or sell underlying securities. This reduces forced trading and allows managers to stay focused on their investment strategies.

Taken together, these advantages do not guarantee outperformance, but they tilt the odds in favor of active managers by removing some of the structural headwinds that have historically worked against them.

All in all, ETFs are uniquely structured to make active investing work.

The Future of Active Management in an ETF World

Looking ahead, the rise of active ETFs could reshape the future of asset management.

As more investors adopt ETF-based portfolios, demand for active strategies within this structure is likely to keep growing. Asset managers are responding by launching new products, expanding into new asset classes, and refining their approaches to active management.

The result is a more competitive and dynamic landscape, where managers must deliver value not only through performance but also through cost efficiency and tax management.

At the same time, the distinction between active and passive investing is becoming less rigid. Investors are increasingly focused on outcomes rather than labels, seeking strategies that align with their goals—whether generating income, managing risk, or enhancing returns.

Popular Active ETFs

These active ETFs, sorted by one-year total returns ranging from 4.7% to 20.6%, carry expense ratios from 0.17% to 0.36%, assets under management from $12.8 billion to $43 billion, and yields from 0.9% to 9.6%.

| Ticker | Name | AUM | 1Y Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| AVUV | Avantis U.S. Small-Cap Value ETF | $22.2B | 20.6% | 1.3% | 0.25% | ETF | Yes |

| DFUV | Dimensional U.S. Marketwide Value ETF | $13.5B | 20.5% | 1.3% | 0.21% | ETF | Yes |

| DFAT | Dimensional U.S. Targeted Value ETF | $12.8B | 19.1% | 1.5% | 0.28% | ETF | Yes |

| DFAC | Dimensional U.S. Core Equity 2 ETF | $41.6B | 17.3% | 0.9% | 0.17% | ETF | Yes |

| JEPQ | JPMorgan Nasdaq Equity Premium Income ETF | $32B | 13.5% | 9.6% | 0.35% | ETF | Yes |

| JEPI | JPMorgan Equity Premium Income ETF | $43.2B | 9.3% | 7.0% | 0.35% | ETF | Yes |

| FBND | Fidelity Total Bond ETF | $24B | 7.0% | 3.8% | 0.36% | ETF | Yes |

| JPST | JPMorgan Ultra Short Income ETF | $36.4B | 4.9% | 4.1% | 0.18% | ETF | Yes |

| MINT | PIMCO Enhanced Short Maturity Active ETF | $14.8B | 4.7% | 4.1% | 0.36% | ETF | Yes |

The growth of active ETFs is not just a trend—it is a structural shift in how investors access active management.

While traditional active mutual funds have struggled to consistently outperform, much of that underperformance can be traced to fees, taxes, and structural inefficiencies. Active ETFs address these issues directly, improving the odds for both managers and investors.

Bottom Line

Active ETFs are improving the odds of success for active managers by removing structural disadvantages—such as higher fees and tax inefficiencies—that have historically held them back. By offering lower costs, greater tax efficiency, and more flexible portfolio management, these strategies allow managers to retain more of their alpha and operate more effectively.

1 Morningstar (March 2026). ETFs Improve Odds of Success for Active Managers