Fixed-income investing is entering a new era. After more than a decade of ultra-low interest rates, heavy central bank intervention, and compressed credit spreads, the bond market looks structurally different. Yields are higher, sector dispersion has widened, and traditional index exposures no longer capture investors’ full opportunity set. The most important shift, however, happens beneath the surface.

Private credit’s rapid rise has been increasingly shaping corporate financing structure, pricing, and trading strategies.

As private lending expands and public markets evolve, the fixed-income landscape has become more fragmented, bringing better opportunities. In this environment, active investment approaches outperform passive strategies by identifying mispricing, managing risk, and capturing income across a broader spectrum of credit assets. Heading into 2026, the case for active fixed-income ties increasingly to the structural transformation from private credit’s ascent.

Private Credit and Regular Bonds

Private credit has shifted from niche institutional allocation to corporate finance’s central pillar. Over the past decade, regulatory changes, banks’ balance sheet constraints, and demand for higher yield have driven non-bank lenders into roles once held by traditional institutions. Private funds now finance leveraged buyouts, middle-market growth, infrastructure, and specialty lending at ever-expanding scale.

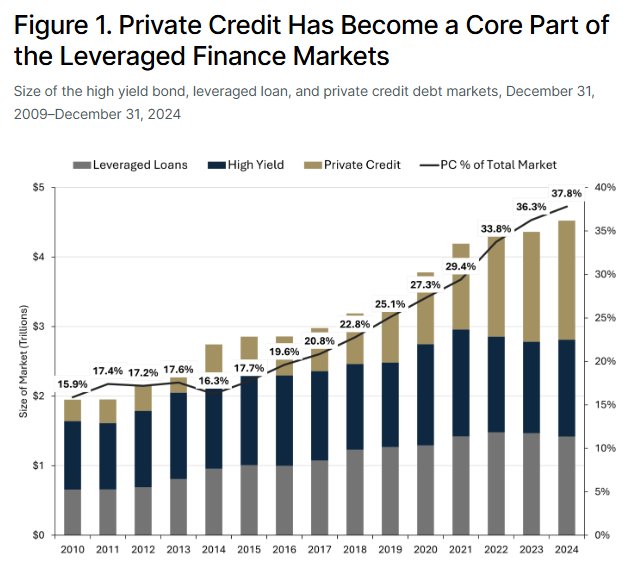

Today, the global private credit market totals $1.7 trillion to $3 trillion, depending on direct lending’s inclusion within the broader private debt ecosystem. That’s a big figure. Private credit has grown so large that it affects the public bond market. It reshapes who issues bonds and who does not. Companies that once tapped high-yield or leveraged loan markets now turn increasingly to private lenders. These borrowers value the flexibility, speed, and customized terms that private credit provides, despite somewhat higher borrowing costs.

This chart from asset manager Lord Abbett highlights private credit’s growth and its significant role in the debt market.

Source: Lord Abbett

This creates gradual segmentation of the credit universe. Riskier or more complex borrowers migrate toward private markets, while larger or more standardized issuers stay in public bond indexes. Meanwhile, private lenders actively manage portfolios, refinance positions, and occasionally shift assets back to public markets. This movement between private and public channels introduces pricing inefficiencies absent to the same degree in earlier cycles.

Mispricing Opportunities

Capital-market fragmentation also fragments information and liquidity. Public bonds trade daily with transparent pricing, while private loans negotiate bilaterally and are priced less often. Assets shifting between markets spawn valuation mismatches, liquidity premiums, and credit-perception gaps.

For example, companies privately financed amid tight bank lending later issue public bonds post-stabilization. Investors comparing new bonds to private valuations may find yield spreads undervaluing improved fundamentals. Conversely, private-portfolio stress sparks public-credit opportunities when forced refinancing or restructurings misprice securities.

Liquidity itself generates returns. Public markets demand extra yield for tradability, while private assets compensate for illiquidity. As capital flows shift between them, spreads widen or compress in ways that reward investors analyzing both environments. Passive index strategies cannot respond to these changes by design, but active managers rotate across sectors, maturities, and issuers to capture relative value.

Private credit’s rise boosts dispersion—and dispersion fuels active management.

Implementing Active Fixed-Income in Portfolios

By contrast, active management evaluates credit fundamentals, liquidity conditions, and structural positioning instead of simply mirroring issuance patterns. This flexibility grows more valuable as private credit alters public bond markets’ composition and behavior.

Managers allocate dynamically across investment-grade credit, high yield, securitized assets, emerging-market debt, and short-duration instruments based on where risk compensation appears most attractive. They adjust duration exposure as interest-rate expectations evolve, emphasize sectors benefiting from economic resilience, and reduce exposure where refinancing risks rise.

Crucially, active strategies incorporate private credit insights even when investing mainly in public securities. Understanding how private lenders structure covenants, price risk, and negotiate terms improves public-market credit selection. Thus, private credit’s growth not only competes with public bonds but also enhances the informational landscape for skilled portfolio managers.

That’s why investors should go active in the year ahead. As private credit grows and mispricing between public and private markets grows more pronounced, active managers prevail.

Multisector Active Bond ETFs

These ETFs offer low-cost exposure to active bond management in unconstrained, dynamic, go-anywhere sectors. Sorted by YTD return—from 7.6% to 9.1%—they have expenses of 0.10%–0.56%, assets of $51M–$22B, and yields of 4.2%–6.8%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| BOND | PIMCO Active Bond ETF | $6.6B | 9.1% | 5.0% | 0.56% | ETF | Yes |

| JCPB | JPMorgan Core Plus Bond ETF | $8.8B | 8.7% | 5.30% | 0.40% | ETF | Yes |

| OBND | SPDR Loomis Sayles Opportunistic Bond ETF | $51M | 8.10% | 6.8% | 0.55% | ETF | Yes |

| FBND | Fidelity Total Bond ETF | $22B | 7.9% | 4.9% | 0.36% | ETF | Yes |

| VCRB | Vanguard Core Bond ETF | $3B | 7.85% | 4.20% | 0.10% | ETF | Yes |

| TOTL | SPDR DoubleLine Total Return Tactical ETF | $4B | 7.84% | 5.1% | 0.55% | ETF | Yes |

| DBND | DoubleLine Opportunistic Bond ETF | $600M | 7.6% | 5% | 0.45% | ETF | Yes |

| BINC | BlackRock Flexible Income ETF | $14B | 7.59% | 5.5% | 0.52% | ETF | Yes |

Private credit’s rise signals more than a cyclical trend—a structural transformation in capital flows through the economy and credit risk distribution between public and private investors. As this transformation unfolds, the fixed-income market becomes less uniform, more dispersed, and more rewarding for those who navigate its complexity.

In this environment, the distinction between active and passive investing sharpens. Passive strategies may serve as low-cost core exposures, but capturing the full opportunity set demands flexibility, research, and judgment—the hallmarks of active management.

Bottom Line

Fixed-income extends beyond interest rates and traditional bond indexes. Private credit’s rapid expansion reshapes corporate financing, fragments liquidity, and creates new relative value pockets across markets. These changes broaden opportunities for investors equipped to respond. Active approaches offer tools to navigate this evolving landscape: