We’ve all heard the old saying, “location, location, location” when it comes to owning real estate. Buildings and properties in prime regions and locations tend to go for more money, have a steady supply of foot traffic and support continuous occupancy. However, when it comes to our portfolios, we tend to take a broader approach with real estate as an asset class.

Since their creation, real estate investment trusts (REITs) have been a wonderful way for both the average Joe and institutional investors to win wide swaths of real estate assets without the hassle of dealing with physical ownership of commercial buildings.

But a broad approach may not be best: Not all property types are doing well, and several are facing long-term downward trends.

In this case, using an active strategy via an ETF could prove to be the best way to gain exposure to real estate and boost returns.

See our Active ETFs Channel to learn more about this investment vehicle and its suitability for your portfolio.

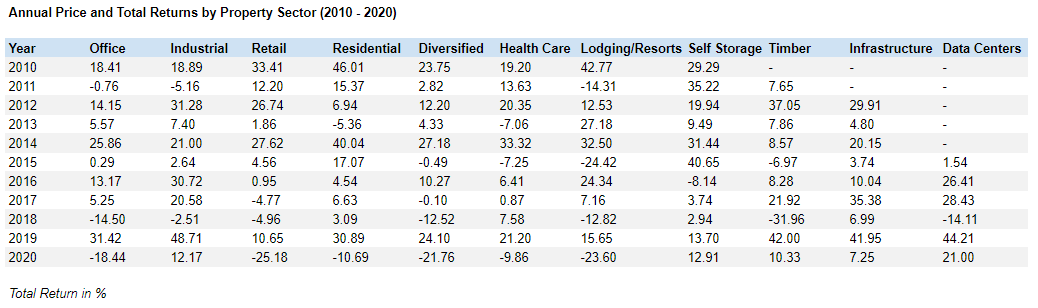

A Difference of Returns

As an amendment to the Cigar Excise Tax Extension of all things, Congress established REITs back in the 1960s, which allowed investors to buy shares in commercial real estate portfolios. In the 1990s, additional amendments allowed these pools to be publicly traded. Since then, the number of REITs and investors using them in their portfolios has exploded – and there’s good reason for this. REITs provide non-correlated assets versus stocks/bonds, and through their tax structure, provide higher-than-average dividend yields.

They also provide great returns. Looking at the FTSE NAREIT All Equity REITs Index,which kicks out mortgage REITs and only focuses on firms that own physical property, total returns for the last 30 years have clocked in at nearly 1,680%. Works out to be just over an average annual return of 10%, this isn’t too shabby at all.

However, digging further into the numbers paints an uneven picture when looking at the various property types, especially over the last decade. And you can see by the following table from NAREIT, some sectors have been more successful than others.

Source: NAREIT

The reasons come down to some long-term trends. Structural changes – courtesy of the Great Recession and COVID-19 crisis – have shifted the winners and losers in the real estate sector. For example, do we need as much office space if work-from-home and remote/mobile environments become the post-pandemic norm? Meanwhile, the “death of the shopping mall” has been reported over and over as retailers embrace online and omnichannel operations.

The reverse has created a different set of winners as well. Rising home prices and increased mortgage lending standards have created surging demands for apartments. Likewise, cloud computing has boosted REITs that own data centers, while warehouses have won due to the surge in e-commerce.

You can really see the unevenness in the returns of various property sub-sectors in the previous NAREIT table.

Better Than Average

Given the diversity in return profiles for various sub-sectors and the long-term trends causing those return differentials, real estate investors could benefit from a dose of active management. Certainly, you can cobble together a portfolio of your own REITs. However, the new surge in active ETF issuance could be a better play on real estate.

Because active managers aren’t tied to any one index, they can pick and choose which property sub-sectors to hold or to underweight. This truly shows the value of “location, location, location.” Take a look at the holdings of the Invesco Active U.S. Real Estate Fund (PSR), which happens to be one of the oldest/first active ETFs on the market, versus the iShares Core U.S. REIT ETF (USRT), which tracks the previously mentioned FTSE NAREIT All Equity REITs Index.

Mall-operator Simon Property (SPG) dominates USRT at 4.45% of assets, and is the third-largest holding. However, in PSR, Simon only makes up 0.89% of assets and isn’t even in the top 25 of the ETF’s holdings. Similarly, the active ETF is weighted heavily in data-centers, warehouses and communication real estate assets – the types of properties which have been winners over the last few years.

The proof may be in the returns. PSR has pretty much matched USRT’s returns since its inception. The only hindrance to its performance has been its expense ratio. However, that could be changing. Like with passive funds, fees on active ETFs continue to drop, including for PSR. The fund’s fee is now a cheap 0.35%.

And PSR isn’t alone in its non-index-tracking ways. There are now several low-cost active real estate ETFs on the market that can “go anywhere” and still own various property types. Over time, these funds should be able to outperform the index by selecting prime locations and various sub-sectors of the real estate market, resulting in better portfolio returns for investors.

Looking for a safe REIT? Check out our recently revamped Best Real Estate Sector Stocks list that relies on our strict Dividend Safety rating system.

The Bottom Line

REITs have been wonderful return generators for investors over the long haul. However, the divergence in returns by property sectors in recent years and unyielding trends mean it may be time to rethink their strategy. In this, active management could be best. And with the launch of active ETFs in the sector, investors now have the ability to focus on the ‘winning’ property types.

Don’t forget to explore our Dividend Guide where you can access all the relevant content and tools available on Dividend.com based on your unique requirements.