Taxes rank among the most persistent obstacles to long-term investing success. While investors focus on picking winners and timing markets, capital gains taxes and taxable distributions erode even strong performance. This “tax drag” significantly reduces after-tax returns, especially in taxable brokerage accounts where every realized gain matters.

In recent years, active exchange-traded funds (ETFs) have emerged as a compelling solution that supports tax-efficient investing without sacrificing professional management.

Despite their advantages, active ETFs are not perfect. Investors seeking to maximize after-tax returns must understand their tax strengths and potential surprises.

Why Active ETFs Tend to Be More Tax Efficient

Given that taxes pervade investing, investors of all kinds continue to tap ETFs, which are inherently more tax-efficient than other vehicles.

Both passive and active ETFs are more tax-efficient than traditional mutual funds, primarily due to their structure.

Unlike mutual funds, which meet redemptions by selling securities for cash and potentially triggering taxable capital gains for all shareholders, ETFs use in-kind creation and redemption transactions to manage flows without realizing gains inside the fund. In an in-kind creation, an authorized participant delivers a basket of the ETF’s underlying securities to the issuer in exchange for ETF shares. The reverse occurs in an in-kind redemption.

ETFs transfer securities directly without selling into the market, so they generate no taxable gains internally and preserve tax efficiency for investors. This mechanism explains why ETFs distribute fewer capital gains than mutual funds.

Investors thus incur capital gains only when they sell shares, making active ETFs a de facto choice for many.

Tax Efficiency in Action—But Not Perfect

Despite these advantages, investors should know that active ETFs remain vulnerable to capital gains distributions and other tax liabilities. ETFs’ structural efficiencies often reduce taxable distributions but do not eliminate tax consequences.

First, when an ETF manager sells portfolio securities for reasons unrelated to shareholder flows—such as tactical rebalancing or strategy shifts—those sales can realize capital gains inside the fund.

Although the creation-redemption process minimizes securities sales for redemptions, actively managed portfolios still produce turnover and realized gains. Without offsetting losses or with unfavorable trade timing, the ETF may distribute gains to shareholders.

Second, some securities or asset classes hinder the in-kind process. Fixed-income instruments, derivatives, and illiquid holdings often require cash transactions that trigger taxable events. Thus, not all active ETFs offer equal tax efficiency as fund structure and the type of underlying holdings matter.

Ultimately, active ETFs are not tax-free.

Morningstar’s 2025 survey of ETF capital gains distributions illustrates this. About 6% of surveyed U.S. ETFs anticipated distributions, with 2% paying significant amounts. 1

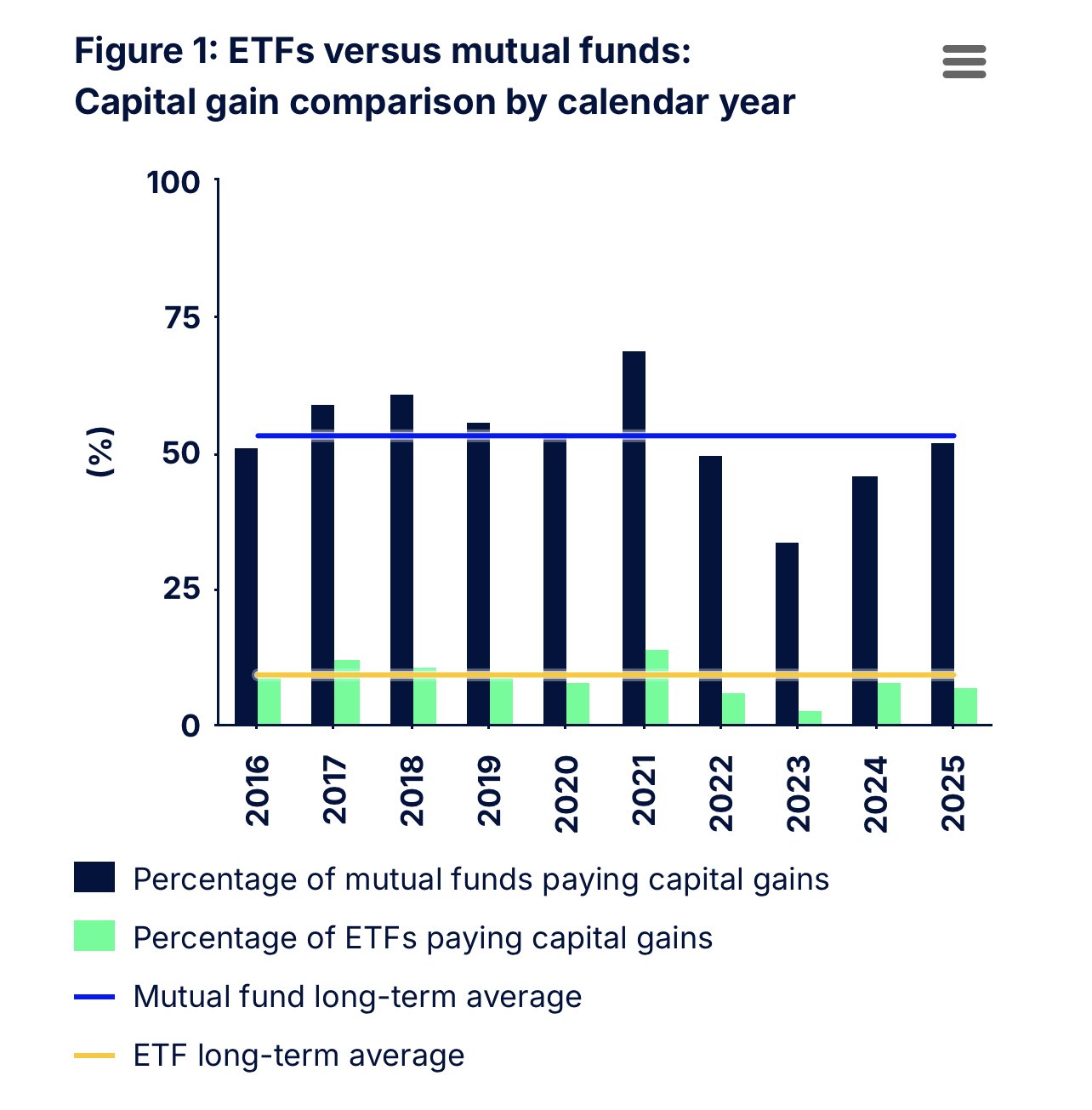

This chart from State Street highlights average gains paid by active ETFs and mutual funds over the last decade.

Source: SSGA.

While active ETFs are tax-efficient, they are not perfect. Capital gains can and do occur.

Putting It All Together for After-Tax Investors

Ultimately, selecting an active ETF for tax efficiency demands more than assuming all ETFs excel at it. One fund may prove more tax-aware than another based on trading frequency, asset class tendencies to produce taxable income or gains, and practices like securities lending that trigger separate tax events.

Investors must weigh all this before buying an active ETF and prepare for tax time to avoid surprises.

Popular Active ETFs

These active ETFs—sorted by YTD total returns (3.1% to 18.4%)—have expense ratios from 0.17% to 0.70%, AUM from $500 million to $42 billion, and yields from 0% to 9.7%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| CGGR | Capital Group Growth ETF | $16.7B | 18.4% | 0.4% | 0.39% | ETF | Yes |

| FBCG | Fidelity Blue Chip Growth ETF | $4.9B | 15.5% | 0.5% | 0.60% | ETF | Yes |

| TCHP | T. Rowe Price Blue Chip Growth ETF | $1.6B | 15.1% | 0% | 0.57% | ETF | Yes |

| DFAC | Dimensional U.S. Core Equity 2 ETF | $38.4B | 11.3% | 0.8% | 0.17% | ETF | Yes |

| JEPQ | J.P. Morgan Nasdaq Equity Premium Income ETF | $30.9B | 11.4% | 9.7% | 0.35% | ETF | Yes |

| DFUV | Dimensional U.S. Marketwide Value ETF | $12.3B | 9.2% | 1.5% | 0.21% | ETF | Yes |

| FBND | Fidelity Total Bond ETF | $21.1B | 7.2% | 4.9% | 0.36% | ETF | Yes |

| HYBL | SPDR Blackstone High Income ETF | $511M | 5.6% | 8.2% | 0.70% | ETF | Yes |

| JEPI | JPMorgan Equity Premium Income ETF | $41.3B | 5.4% | 7.4% | 0.35% | ETF | Yes |

| JPST | JPMorgan Ultra Short Income ETF | $34.1B | 4.4% | 5.2% | 0.18% | ETF | Yes |

| AVUV | Avantis U.S. Small-Cap Value ETF | $18.6B | 4.1% | 1.4% | 0.25% | ETF | Yes |

| MINT | PIMCO Enhanced Short Maturity Active ETF | $14B | 4.1% | 5.3% | 0.35% | ETF | Yes |

| DFAT | Dimensional U.S. Targeted Value ETF | $11.6B | 3.1% | 0.8% | 0.28% | ETF | Yes |

For investors in taxable accounts—particularly those in higher tax brackets—the difference between active mutual funds and active ETFs can prove substantial, as fewer capital gains distributions keep more investment growth in your pocket.

However, active ETFs are not “tax-free.” Internal trading, turnover, asset types, and fund structures can trigger gains distributions. Investors seeking tax efficiency should evaluate not only the ETF wrapper but also turnover management, historical distributions, and security types.

Bottom Line

Active ETFs offer tax-aware investors a structural advantage with fewer capital gains distributions than traditional mutual funds, thanks to their creation-redemption mechanism. However, they remain vulnerable to turnover, strategy-driven trades, and unexpected capital gains.

1 Morningstar (January 2026). Few ETFs Project Capital Gains Distributions in 2025: Key Takeaways for Investors