For much of the past decade, investors have had little reason to look beyond U.S. growth stocks. The rise of mega-cap technology companies, the dominance of artificial intelligence (AI)-related themes, and the extraordinary performance of a handful of market leaders have created one of the strongest periods of growth stock outperformance in modern history. As a result, many investors have become increasingly concentrated in U.S. equities and, more specifically, a relatively small group of large-cap growth companies. This concentration, however, has increased the opportunities in many forgotten asset classes.

In this environment, international value stocks could be one of the most compelling opportunities.

International value stocks rarely generate headlines and generally lack the excitement of AI, cloud computing, and disruptive technology. However, these firms offer investors ample benefits, including increasingly strong returns and income potential.

How International Value Became the Forgotten Asset Class

The underappreciation of international value stocks did not happen overnight.

Following the Global Financial Crisis, a combination of factors favored U.S. growth companies. Low interest rates rewarded long-duration growth assets, and technology became an increasingly dominant part of the global economy. The U.S. emerged as the home of many of the world’s largest and most profitable technology firms. Meanwhile, international markets faced headwinds, including slower economic growth, political uncertainty, and weaker currency performance relative to the U.S. dollar.

As investor capital flowed toward U.S. growth strategies, international value stocks increasingly fell out of favor.

The result has been a significant shift in investor allocations. Many portfolios today are heavily concentrated in U.S. large-cap growth stocks with relatively little exposure to international value, and in some cases investors have effectively abandoned the asset class altogether.

Today, dedicated international value allocations hold the lowest market share of any style type—down to the single digits, according to Morningstar data. 1

Opportunity Among the Neglected

Ironically, this neglect may be creating opportunity.

Financial markets often reward investors willing to look beyond the most crowded trades. While growth stocks have generated impressive returns, they have also become increasingly expensive. International value stocks, by contrast, continue to trade at discounts that would have seemed extraordinary just a few years ago.

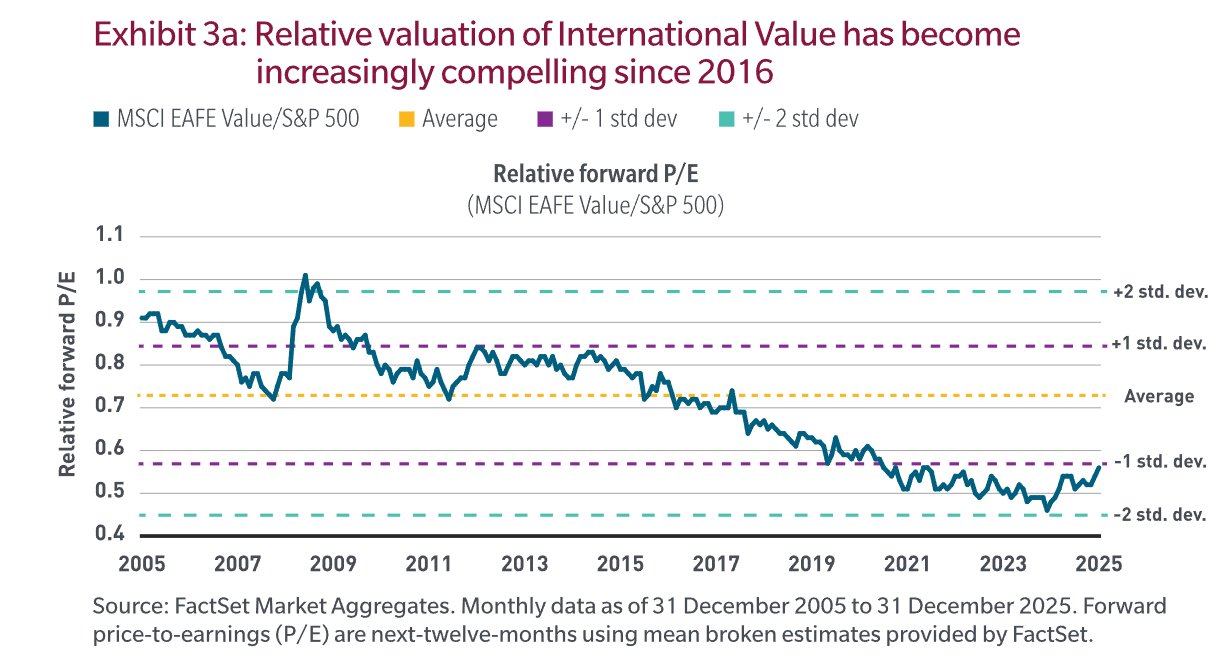

Many international markets continue to trade at substantial discounts to U.S. equities, particularly relative to the market’s most expensive segments. Value-oriented sectors abroad often trade at earnings multiples well below those of U.S. growth companies. When comparing the MSCI EAFE Value Index to the S&P 500, international value stocks are trading at valuations well below historical norms. This chart from MFS highlights the continued decline in the “cheapness” of foreign value.

Source: MFS

What’s interesting is that those valuations haven’t dropped solely due to being unloved by investors—earnings have improved as well. Many sectors that populate international value indexes, including financials, industrials, energy, materials, and consumer staples, have continued to generate meaningful profits.

Financial companies have benefited from higher interest rates and improved profitability, while industrial firms are participating in infrastructure investment, reshoring trends, and global capital spending. Energy and materials companies continue to benefit from structural supply constraints and disciplined capital allocation. Consumer-focused firms have prospered in many emerging markets, such as China, that look beyond U.S. goods to address trade issues. These positive earnings trends appear durable and have the potential to continue in the years ahead.

Another positive for international value is its mix of companies relative to U.S. markets, which creates a stronger diversification play for portfolios. According to MFS, the MSCI EAFE Value now trades at a 0.54 correlation to the S&P 500, versus 0.69 for the broader MSCI EAFE—very low by historical measures and a real opportunity for investors to add non-correlated assets to their portfolios.

The diversification also extends to additional benefits when considering currencies and economic drivers.

Then there are dividends to consider. Many international companies have historically maintained stronger dividend cultures than their U.S. counterparts, with firms in Europe, Japan, Australia, Canada, and other developed markets often prioritizing returning cash to shareholders rather than emphasizing rapid reinvestment or share price appreciation alone. This has created an asset class that tends to offer higher dividend yields than many U.S. growth-oriented strategies and, more importantly, has lowered the volatility of international value while providing a smoother ride for portfolios.

History Suggests Investors Shouldn't Ignore International Value

As if the overall cheapness and diversification benefit weren’t enough reason to consider international value, returns sweeten the pot.

MFS research shows that today’s environment closely resembles the Dotcom Boom/Bust, with similar rates of inflation, 10-year yields, international stock valuations, and U.S. tech valuations. While history doesn’t repeat, it does rhyme. From January 2000 through December 2007, the MSCI EAFE Value Index crushed the S&P 500 with an annualized return of 8.2% vs. 1.7%, while the U.S. technology sector produced a negative 7.7% annual return over the same period.

Given this potential to regain the lead amid cheap valuations, international value is starting to look like a strong portfolio addition. Despite the unloved nature of these stocks, investors have ample ways to gain exposure, and ETFs offer a simple, efficient path to the asset class without requiring individual security selection or direct navigation of foreign markets.

Broad international value ETFs provide diversified exposure across developed markets, including Europe, Japan, Australia, and Canada. Investors can also find products focused on specific regions, countries, or factor-based approaches that emphasize valuation, quality, and dividend characteristics. Numerous active options are now available as well, offering the potential for additional alpha.

International Value ETFs

These ETFs provide exposure to international value stocks through either active or passive management. Sorted by year-to-date total return (from 10% to 22%), they feature expense ratios between 0.18% and 42% and AUM ranging from $533M to $30B. They are currently yielding between 2.4% and 3.8%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| FNDF | Schwab Fundamental International Equity ETF | $23.11B | 22.03% | 2.83% | 0.25% | ETF | No |

| AVDV | Avantis International Small-Cap Value ETF | $18.92B | 16.89% | 3.65% | 0.36% | ETF | Yes |

| FIVA | Fidelity International Value Factor ETF | $532.89M | 13.36% | 2.51% | 0.18% | ETF | Yes |

| AVIV | Avantis International Large Cap Value ETF | $1.27B | 12.39% | 3.75% | 0.25% | ETF | Yes |

| DFIV | Dimensional International Value ETF | $19.32B | 12.32% | 2.54% | 0.27% | ETF | Yes |

| DISV | Dimensional International Small Cap Value ETF | $4.64B | 12.02% | 2.38% | 0.42% | ETF | Yes |

| EFV | iShares MSCI EAFE Value ETF | $29.97B | 9.98% | 3.79% | 0.31% | ETF | No |

International value stocks spent much of the last decade in the shadows as investors chased the remarkable success of U.S. growth companies, yet market history suggests that periods of extreme concentration and valuation divergence rarely last forever.

Today, international value offers several characteristics investors often seek but struggle to find simultaneously: attractive valuations, growing earnings, strong dividend income, and meaningful diversification. With many portfolios heavily concentrated in a narrow group of expensive growth stocks, the asset class may serve as both a potential return source and an important risk-management tool.

Bottom Line

International value stocks may not generate the excitement of AI, mega-cap technology, or the latest growth trend, but they offer a combination of attractive valuations, improving earnings, strong dividend income, and meaningful diversification that is increasingly difficult to find elsewhere.

1 MFS (March 2026). International Large-Cap Value: The Forgotten Asset Class