Junk bond yields are hovering around 8.47% (and more for lower-rated issuers), but experts have little consensus on whether to invest. Meanwhile, the issuance of junk bonds fell from $13.9 billion in February to $4.45 billion in March as the market’s appetite for risk shrunk. As a result, you may be wondering if it’s a good time to invest.

In this article, we’ll look at what risks remain for junk bonds over the coming months and why some asset managers are eager to buy.

Don’t forget to check our Fixed Income Channel to learn more about generating income in the current market conditions.

Junk Bonds Remain a Risky Bet

The Silicon Valley Bank collapse and concerns about regional banks have led to low credit availability. During regular times, lower credit availability leads to higher interest rates as borrowers face higher standards. And when you add in the potential for a recession, these interest rates typically soar even higher to compensate for the risk.

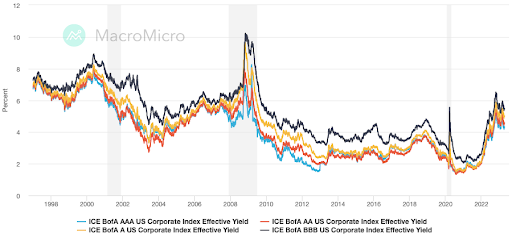

Currently, AAA-rated corporate bonds are yielding 4.34%, whereas B-rated bonds trade at 8.47%, and CCC and lower-rated bonds trade at 14.70%. While the spreads between these bonds and Treasuries are widening quickly, the spreads between AAA and junk bonds remain historically tight (see the chart below).

AAA vs. BBB-rated corporate bond spreads remain historically tight. Source: MacroMicro

The consensus is that credit spreads must widen further, given the lower credit availability and risk of a recession. If a recession occurs, many smaller borrowers could see less cash flow and may have trouble servicing their debt. CCC-rated and lower debt in particular could see a jump in defaults if a recession materializes.

Don’t forget to explore all High Yield Bonds to see if they suit your portfolio needs.

But a Recovery Could Pay Off

A handful of asset managers remain bullish on junk bonds despite these risks. For instance, JPMorgan Asset Management said on March 27 that it would add exposure to high-yield credit when the time is right. The goal is to stock up on sectors that could outperform when the economy returns to growth, capitalizing on today’s high yields.

In particular, JPMorgan’s asset managers suggested they would buy mining and autos in the BB-rated high-yield space. However, they quickly noted that spreads need to widen, and there needs to be more decompression of spreads between investment-grade and high-yield before they make any significant moves.

Investors who wish to start building exposure to junk bonds earlier can also consider actively managed ETFs rather than passive funds. For example, the Invesco High Yield Bond Factor ETF (IHYF) uses a factor-based strategy to outperform market-weighted indexes, incorporating fundamental and technical factors into its decisions.

The Bottom Line

Junk bonds are offering juicy yields in today’s market, but the spread between AAA-rated and junk bonds remains tight. As a result, most asset managers are waiting on the sidelines until these spreads decompress before adding exposure to their portfolios. However, signs of economic improvement could produce bargains in the space.

Take a look at our recently launched Model Portfolios to see how you can rebalance your portfolio.