The COVID-19 pandemic has taken a massive toll on the global economy. While unemployment remains stubbornly high, the Federal Reserve’s monetary policy actions and the federal government’s early fiscal stimulus helped stabilize the capital markets. The big question is whether these fiscal stimulus measures will continue and when the economy will recover.

Let’s take a look at how COVID-19 has impacted the mortgage-backed securities market and where investors can look for opportunities.

Don’t forget to check out our Fixed Income Channel to learn more about fixed income concepts and trends.

Impact of COVID-19 on MBS

The arrival of COVID-19 in the United States had a swift impact on the financial markets. In March, investors began liquidating stocks and bonds across the board, which sparked an overnight liquidity crisis. Funds that dealt in relatively illiquid assets, such as mortgage-backed securities, were forced to dramatically scale down their holdings in short order.

For instance, the AlphaCentric Income Opportunities Fund (IOFIX), which focuses on lower-rated mortgage-backed securities, fell by more than 30% in just a week and was forced to put up $1 billion worth of securities for sale. Commercial real estate operators, such as WeWork, also had their credit ratings cut due to an anticipated shortfall in cash flow.

Of course, the Federal Reserve stepped in with a pledge to provide up to $2.3 trillion in loans to support the economy in April and continues to purchase about $120 billion per month of Treasury and mortgage-backed securities in the open market. These efforts – combined with robust fiscal support – helped stabilize the markets and return them to an upward trajectory.

Be sure to check bond funds section to explore various funds from the fixed income space.

Robust Fundamentals

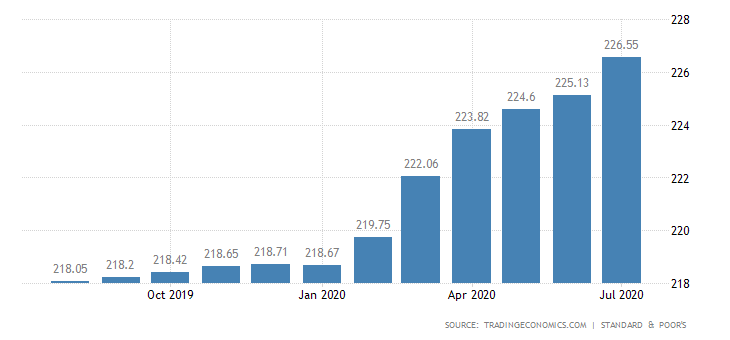

The housing market has been surprisingly resilient in the face of COVID-19. After starting 2020 with substantial momentum, housing inventories hit new lows and spurred record-high home prices in many regions. The Case-Shiller Home Price Index rose 3.9% in July versus a year ago following a 3.5% increase in the previous month and surpassing estimates for 3.8% growth.

Despite high levels of unemployment, aggregate consumer fundamentals remain strong with the ratio of consumer financial obligations to disposable income reaching 20-year lows. Falling interest rates and rising incomes are responsible for these trends, particularly as refinancing activity has experienced a sharp increase over the past several months.

That said, these fundamentals are dependent on continued fiscal support. Mortgage delinquencies rose during the second quarter to a seasonally adjusted rate of 8.22% of all loans outstanding, according to the Mortgage Bankers Association’s National Delinquency Survey, suggesting that the expiration of fiscal stimulus and protections could impact the market.

Sorting Risks From Opportunity

Actively managed mortgage-backed securities funds have been the strongest performers given their ability to identify securities with low prepayment risk and strong fundamentals. By focusing on conventional MBS versus Gennie Mae-issued securities, these funds have been able to select coupons and collateral stories with more predictable prepayment profiles.

Commercial MBS has a bit more uncertainty. While Class A properties with well-capitalized sponsors may be able to cope with the pandemic, hotels, retail properties and Class B/C properties are a lot riskier. Actively managed funds are well-suited to analyze these risk factors and optimize a portfolio to minimize default risks over time.

Despite concerns over prepayments or fundamentals, many analysts expect the MBS market to continue to outperform Treasuries into the third quarter. Strong demand from investors seeking high-quality yield, ongoing support from the Federal Reserve and ongoing strength in home prices are likely to offset delinquencies and any increases in supply in the near term.

The Bottom Line

The COVID-19 caused a liquidity crunch across the capital markets, but swift fiscal and monetary interventions thwarted any disasters. While there are subsets of the market that are struggling, most analysts agree that strong underlying fundamentals in both the housing market and consumer debt ratios bode well for the immediate future.

Over the long term, investors should keep a close eye on ongoing fiscal support for homeowners to avoid delinquencies and ongoing improvements in the job markets. With net supply growth remaining slow, the underlying housing market could continue to see strength over the intermediate term given the low interest-rate environment.

Be sure to check out our News section to be up-to date with trending funds and market updates.