It seems we are facing a bit of a retirement crisis. We have all read and heard the rumors that we aren’t saving enough to help power our golden years. That part we know. However, the way we are saving could actually be the problem.

I’m talking about our humble 401(k) plans.

The plan is a thing of beauty – allowing workers to stash a ton of cash away, tax deferred. Heck, most of us even get a match on our contributed dollars from our employers. However, even as awesome as the 401(k) is, it may not be doing the trick versus the old retirement standby – pension plans. New studies show just how much of a discrepancy there is.

6-To-1 Difference

It’s no secret why pension plans are on the way out at many corporations and even state agencies. The private entities simply don’t want the future liability on their books. Defined contribution plans – 401(k), 403(b) and 457 – push the liability onto the retiree. In exchange for now shouldering that burden, you and I are able to get a match on our savings from our employers, lower taxes and the ability to shelter assets until we are 70 years old.

The problem is that most workers aren’t using the 401(k) effectively, and new studies show that to be a fact.

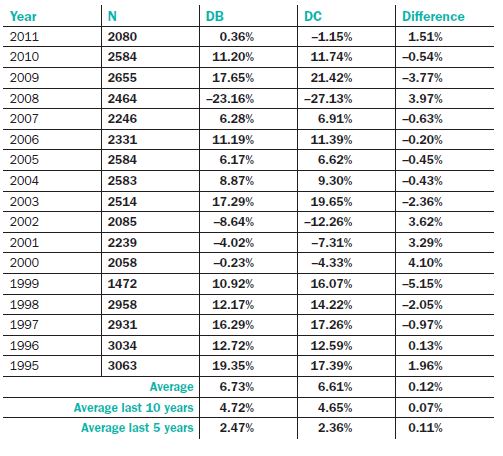

According to an analysis by Boston College researchers, private-sector pension funds – not government-sponsored plans – produced annual returns that were 0.7% higher than employees’ 401(k) plans from 2000 to 2012. For the 12 years analyzed by Boston College, pensions managed to produce returns of 6.6% versus the 5.9% realized by defined contribution plans, like 401(k)s and 403(b)s.

This echoes a similar study from Towers Watson that pushed the starting year back to 1995. The extra return from a pension plan was nearly the same, and pensions managed to outperform defined contribution plans annually. See the table below.

What’s more is the average 401(k) or rollover isn’t cutting it on the income front either.

The nonpartisan Economic Policy Institute’s work showed that the average 401(k)/rollover balance was able to generate just $1,000 in average annual distributions. The same amount of assets in a pension was able to generate nearly $6,000 annually during its study.

The Reason for the Difference

The rationale behind the difference comes down to a few different factors. For starters, there’s the automatic nature of pensions. There are no options. They are called “defined benefit” plans for a reason. If you want X, you must contribute Y. Employees entering a pension plan are only signing up for their plan. 401(k)s are 100% optional, and most workers either aren’t contributing enough or even at all.

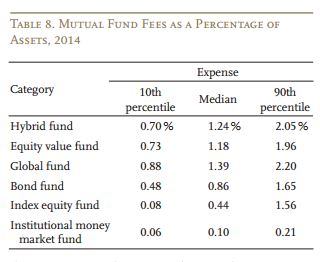

Second is fees. The vast bulk of defined contribution plans are set up using mutual funds, and active ones at that. The management fees can prune down balances faster than poor market performance. The more you keep, the better your returns are. Boston College illustrates the difference in fees.

The Problem for Most of Us

The problem for most of us is that we don’t have a pension plan and the guaranteed income it brings. In 1980, about 38% of us did. However, that number today has dropped to less than 15%. What that means is that we need to do some of the legwork.

The obvious play is to save more. With the average worker only saving 7.3% in their 401(k), there’s still plenty of room for improvement. Especially since most advisors recommend you save 15% per year. Shoot for the max – currently $18,000 – or at bare minimum increase your contribution each year by a set percentage, till you hit that 15% mark.

Second, look to control costs wherever you can. If you have access to index funds, those sorts of funds typically have lower expense ratios than actively managed ones. The less you pay in fees, the more you’ll have at retirement time.

Finally, be smart with accounts outside your 401(k). Adding funds to an individual retirement account (IRA) can be a great move. More importantly, focusing on dividend stocks and those that can throw off some income/yield will go a long way to helping bridge the gap between a 401(k) and a pension fund. After all, getting 3-4% in yield takes a lot of the guesswork out of reaching for returns. (Are dividend stalwarts that great? Click on Are the Aristocrats, Kings & Champions Really Worth Following? to find out!)

The Bottom Line

In reality, going alone may actually be hurting us on the returns and retirement income fronts. While pensions also have their flaws, they eliminate many of the problems facing 401(k) savers – but knowing about those problems is the first step. In the end, we simply aren’t using our 401(k)s, and other defined contribution plans, effectively.

Saving more is the only answer.