Kraft Heinz Company (KHC ) is the result of a huge merger worth approximately $45 billion between two global consumer products giants, Kraft and Heinz. The deal received heavy approval from Heinz shareholders, including Warren Buffett, Chairman of Berkshire Hathaway (BRK.B). Berkshire Hathaway was a major Heinz stockholder, and now owns roughly 325.5 million shares of Kraft Heinz.

On July 6, 2015, the combined entity began trading on the NASDAQ. The merger brought together two large companies that have now created an industry conglomerate. Kraft Heinz’s major brands include Kraft, Heinz, Jell-O, Maxwell House, Ore-Ida, Oscar Mayer, Planters, Plasmon, Velveeta and many more. In all, it is the fifth-largest food and beverage company in the world. The combined company produces more than 200 brands that are sold in over 200 countries across the world. Of these brands, eight generate more than $1 billion each in annual revenue. And, some of Kraft Heinz’s brands have been manufactured for more than 100 years.

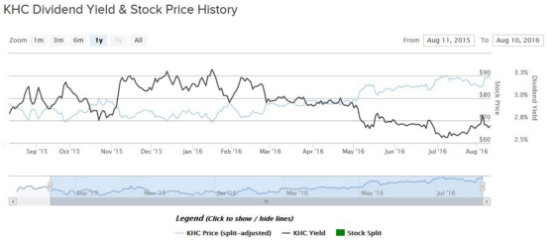

Kraft Heinz stock has performed very well since the merger. Based on its Aug. 11 closing price of $89.44 per share, the stock has returned 15% in the past one year, not including dividends. This has beaten the performance of the S&P 500 Index, which is up 5% in the same period. Kraft Heinz stock is currently at its 52-week high.

High Earnings Growth Potential

One big reason why Kraft’s and Heinz’s stockholders were in high favor of the deal is because of the significant earnings growth presented by the merger. This is why the stock has performed so well since the merger. Going forward, Kraft Heinz has the potential for rapid earnings growth. Since Kraft and Heinz were such similar companies, the complementary nature of the two brand portfolios and business models offered the opportunity for significant cost synergies. There are many duplicated functions between the two companies – in manufacturing and distribution – that can be eliminated, without sacrificing revenue growth. These gains will come quickly, as the two companies expect the merger to be accretive to earnings as soon as next year. This is why analysts expect Kraft Heinz to grow earnings next year by 24%, to $3.82 per share.

The merger has already brought significant growth in profits. Last quarter, Kraft Heinz reported 39% growth in adjusted earnings per share. Adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) soared 23% on a constant-currency basis. These gains came despite the fact that Kraft Heinz’s organic revenue, which measures sales after excluding currency fluctuations, declined 0.5% last quarter.

As a global company, Kraft Heinz is seeing pressure from foreign exchange. The rising U.S. dollar over the past year has made exports less competitive, and it reduces the value of revenue generated in international markets. Because of unfavorable currency fluctuations, Kraft Heinz’s revenue was reduced by 4% last quarter alone. Fortunately, the company is making up for this with significant cost-cutting and price increases. Kraft Heinz raised prices last quarter, which added 1.6% growth to revenue for the period. The biggest pricing gains were in the United States, Canada and the Rest of World (RoW) international region. This is a good sign that underlying demand for Kraft Heinz products remains strong, and that the company still enjoys pricing power.

The currency headwind will likely be short-term over long-term, and focusing on international markets for growth is a wise strategy. That is because emerging markets present far more growth potential to a consumer products company like Kraft Heinz than more developed markets, like the United States. For example, last quarter Kraft Heinz realized 5% pricing increases in the Rest of World segment, which comprises all countries where Kraft Heinz operates outside the U.S., Canada and Europe. This fueled 7.1% organic revenue growth in this segment last quarter, and growth rates moving forward should continue to be high.

The worst-performing segment for Kraft Heinz right now is Europe, where organic sales declined 2.3% last quarter. That is not surprising, given the economic uncertainty presented by the recent Brexit vote. Fortunately, Kraft Heinz derives less than 10% of its revenue from Europe, so this risk is manageable and should not significantly affect the company.

Dividend Growth

With strong earnings growth potential, Kraft Heinz should be able to reward shareholders with rising dividends each year. For example, on Aug. 4, the company announced that its Board of Directors approved a dividend increase. The new quarterly dividend rate will be $0.60 per share, which is a 4.3% increase from the previous quarterly rate of $0.575 per share. This dividend is payable on Oct. 7, 2016, to shareholders of record as of Aug. 26, 2016. The annualized dividend will rise to $2.40 per share. Based on the Aug. 11 closing price of the stock, the current dividend yield rises to 2.7%, which is above the average dividend yield in the S&P 500 Index of approximately 2%.

The company passed through a relatively modest dividend increase, considering it maintains a modest payout ratio. Kraft Heinz’s new $2.40 per share annual dividend still represents 63% of 2017 expected earnings. Continued growth should give the company plenty of room to raise its dividend by 6-8% per year. Assuming 7% annual dividend growth, Kraft Heinz investors will see significant increases in dividend income.

Five Year Projected Annual Dividend Growth

The Bottom Line

Kraft Heinz is a highly profitable company with a strong product portfolio filled with industry-leading brands. It has a global reach and should generate significant earnings growth going forward, thanks to cost cuts, price increases and growth in new international markets. The stock has performed very well since the merger, and its current 2.7% dividend yield is attractive for income investors.