The impact of data and technology on our investment decisions has elevated the role of factors in everyday decision-making. While the concept behind factors isn’t new, portfolio managers in recent years have been compelled to re-evaluate the foundations of successful asset allocation.

What Are Factors?

Factor investing refers to a broad area of investment research that elevates the role of factors in portfolio management. As Fidelity notes, factors such as “size, value, momentum, quality and low volatility” are among the most important when constructing “smart” or “strategic” beta strategies. By focusing on these characteristics, investors can enhance the size of their returns over time.

The type or blend of factors deployed by investors depends largely on their risk tolerance and underlying objectives. Factor-based strategies have been known to help investors improve returns and lower risk over long-term horizons. This is true of single-factor strategies as well as those seeking exposure to multiple factors at the same time.

Portfolios gain exposure to factors through a combination of historical analysis, selection, weighting and rebalancing in favor of assets that meet certain characteristics, such as enhanced risk-adjusted returns or low volatility. In practice, investors can gain exposure to factors through quantitative, actively-managed funds.

Learn here about choosing the right commodity mutual fund.

Types of Factor Investing

In general, there are two main types of factors that have produced favorable returns: macroeconomic factors and style factors.

Macroeconomic factors capture broad risks across asset classes. They include things like economic growth, interest rates, inflation and emerging markets.

Style factors are used to help explain returns and risks with specific asset classes. Things like value, momentum, minimum volatility, quality and size are all examples of style factors.

While there are several actively-managed mutual funds that offer factor investing, exchange-traded funds (ETFs) are the vehicle of choice for most investors. This holds true despite the fact that some mutual funds offer higher factor exposure than smart-beta ETFs. There could be many reasons why investors prefer ETFs over mutual funds, but the most likely explanation is the relative underperformance of factor-based mutual funds compared to their ETF counterparts. Higher fees are another reason why ETFs are more popular.

That being said, factor investing through mutual funds is still a worthwhile endeavor, depending on your investment goals. The Vanguard U.S. Multifactor Fund Admiral Shares (VFMFX) and the Global Minimum Volatility Fund Admiral Shares (VMNVX) are two prominent examples.

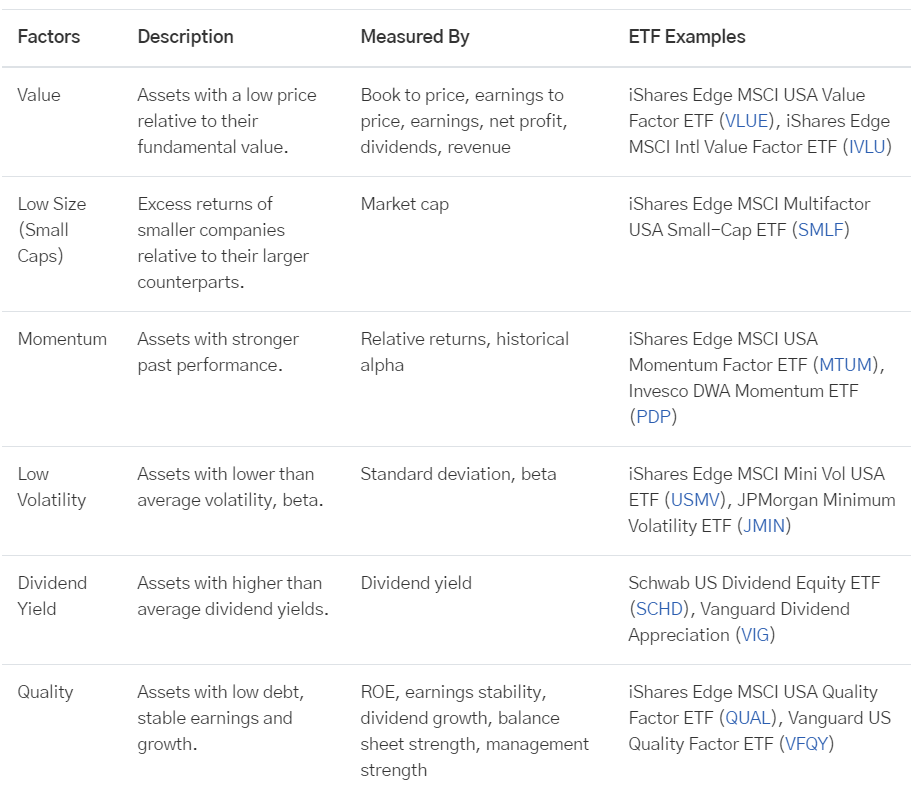

Below is an illustration of so-called systemic factors, which form the basis of most factor-based strategies. As you can see, most of these fall under the umbrella of style factors.

Read more on if mutual funds successfully adopt factor investing here.

Benefits and Drawbacks of Factor Investing

Like any investment approach, factors present market participants with benefits as well as drawbacks. In terms of benefits, factor-based strategies have been shown to provide targeted access to factor exposures. Basically, this means that the ETF examples presented above (as well as many others) actually do what they say they do. If you are targeting dividend yield, ETFs that provide exposure to that factor will produce the desired results. The same holds true for momentum, low volatility or other factors not presented above.

During the height of the bull market in 2017-18, every factor except value was outperforming the market. However, factors such as momentum are hit-and-miss. Momentum was the best-performing factor in 2017, but it has offered no aggregate value over the previous ten years because of the financial crisis in 2008-09. As such, factor investing can be highly cyclical and prone to fluctuations.

Additionally, research from Robecco Institutional Asset Management found excess returns for low-beta, value and small-cap funds but no consistent returns for momentum and reversal funds.

In terms of other advantages, many factor-based strategies provide exposure to multiple factors within one vehicle, which gives investors a better shot at achieving their desired outcomes. Additionally, factor-based models represent a broad universe, which means diversification across many asset classes and factors is possible. Finally, advances in technology and data analysis allow investors to take advantage of factor-based models using more enhanced tools and processes.

On the opposite side of the spectrum, factor investing has a few notable drawbacks. For starters, no single factor works all the time. In fact, returns tend to be cyclical, which means extended periods of underperformance are possible and even likely. What’s more, the market for factor-based strategies has become more crowded in recent years, making it more difficult to pick out funds that will produce the desired results. Poorly constructed strategies can actually give you unintended exposures to factors you did not target initially. And because these strategies are actively managed, you can expect to pay more in terms of management fees.

Be sure check our News section to keep track of the recent fund performances.

The Bottom Line

Recent advances in technology and data science have made factor investing all the more compelling. Investors in the market for actively-managed funds should strongly consider these approaches to enhance long-term results.

Sign up for our free newsletter to get the latest news on mutual funds.