We often hear that saving money is the hard part. Steadily putting money away for years, and even sometimes decades, takes plenty of discipline. However, turning that pool of savings into a stream of income could actually be even more difficult. This is especially true given some of the forces at work. In this case, we’re talking about the invisible hand of rising inflation.

Inflation can wreak havoc on even the most carefully laid out retirement plans. Turning a dollar’s worth of savings into just pennies, inflation is a major factor retirees face throughout their entire golden years.

And with measures of inflation recently running higher and closer to historic norms, retirees need to be vigilant about the market force and preventing/limiting its effects on their savings as well as their lifestyle.

Keep track of the latest news in our News section, where we regularly publish the latest around dividend investing.

A Current Move Higher…

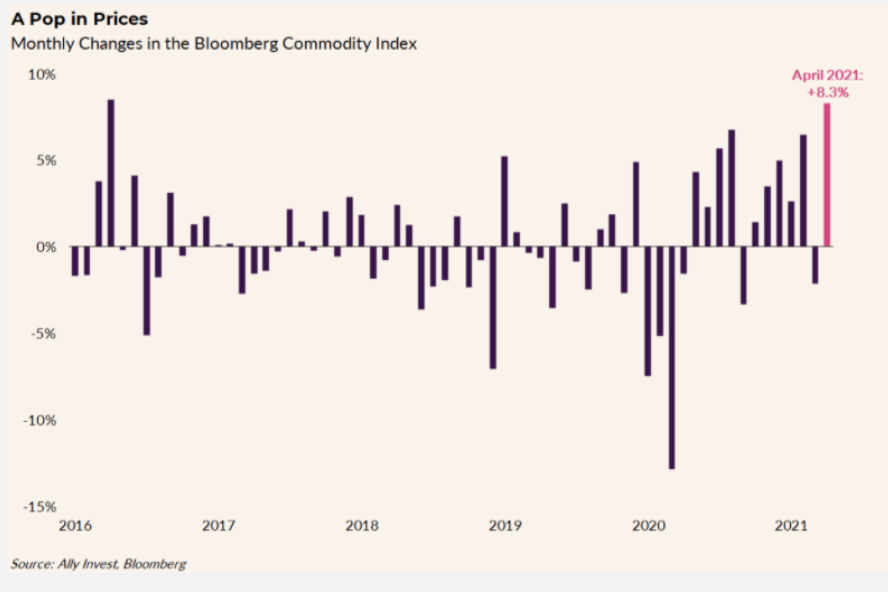

If you’ve left your house post-pandemic, you may have noticed that you’re paying more for your cup of coffee, prescription medicines and to fill up your tank of gas. Thanks to a variety of factors, inflation has steadily risen since the start of the year. The Core Consumer Price Index (CPI), which measures food and energy prices, showed a 3.8% year-over-year growth in May. This was the fastest increase since 2008. Adding in food and energy, we’re looking at a 5% jump in inflation. Measures of both producer and services inflation have also shown big increases over the last year.

This is evident in the chart below from Ally Invest, Bloomberg.

Source: Ally Invest, Bloomberg

…Can Lead to Big Problems for Retirees

This is a problem for all consumers and savers. But it’s particularly a problem for those living off of their savings. In theory, workers can – and do – receive cost-of-living adjustments/raises from their employers. This goes a long way to help keep their spending power high. However, that’s not necessarily true for those living in their golden years.

Simply put, available spending power decreases thanks to inflation.

For example, Rachel diligently saves $6,000 per year over 30 years for her retirement. Earning a 7% return, she’ll have a nest egg worth about $606,000 – not too shabby at all. However, over that period of time, inflation averages just 2%, reducing her purchasing power of that savings to just $334,000. Sure, Rachel will still have over $600k, but what that amount can buy will also be reduced. The cost of milk, gasoline, housing, etc., will all be higher once Rachel retires. If inflation runs at 3%, which is closer to the long-term average, Rachel’s savings would only buy about $250,000 worth of goods. Gulp.

For someone who isn’t earning new dollars via employment, inflation can seriously be a real issue. Even a decent sized nest egg will be diminished as prices rise over time. The scary part is that prices for some goods and services like energy costs and healthcare increase at faster rates than the headline CPI.

Learn about Treasury Inflation Protected Securities (TIPS) here.

You Can Fight Inflation

With even small increases to inflation hindering purchasing power, retirees need to focus on minimizing its effects to their lifestyle and purchasing power. No one wants to run out of money or have to give up their weekly golf game because their portfolio can’t keep up with pricing pressures. To fight inflation, retirees may need to think outside the box a bit.

Fixed income investments and bonds have long been a top draw for retirees. They’re safe – especially U.S. Treasury bonds – and they provide a steady interest payment. The problem when it comes to inflation is that these coupons are fixed. You earn the same amount of money each time you’re paid. But thanks to inflation, each year that coupon payment is worth less in terms of purchasing power. Sure, you’ll get $1,000 in interest payments, but by year two that $1,000 would only buy $980 worth of goods.

You shouldn’t abandon fixed income investments as they do have benefits for a portfolio, but leaning on them heavily isn’t a good idea. They won’t stop inflation.

Having more of your portfolio in dividend stocks could be the answer. Aside from the capital appreciation potential, dividend stocks tend to raise their payouts each year. Better still is that this rate has long eclipsed CPI. Historically, the rate at which stocks in the S&P 500 have increased their dividends per year has been just under 6%. That in of itself goes a long way in fighting the effects of inflation on a portfolio. At the same time, total returns for dividend growth stocks have been robust during periods of inflation. As shares raise payouts, investors have historically flocked to these stocks to take advantage of the higher income. The inflation-fighting effect is compounded.

There are other ways to fight inflation as well.

Protecting cash and short-term spending needs from inflation can be done as well. But Treasury Inflation Protected Securities (TIPS) and I-bonds have special “boosts” to their coupon rates designed to keep up with rates of the CPI. Here, investors can protect a portion of their near-term spending needs from price increases. And in the case of I-bonds, there are some pretty decent tax deferrals as well.

Finally, even adding a dose of commodities can be worth your time. Corn, oil, gold, etc., are often directly correlated with rises to the CPI. Having a swath of commodity exposure in your portfolio makes sense to fight back rising prices. And it’s easy too. Thanks to a variety of exchange-traded funds (ETFs) adding a dose of commodities to a portfolio has never been simpler.

The Bottom Line

Inflation is a major force that retirees have to face head-on if they want to be successful. The invisible hand of rising prices can act like a grenade on even the most carefully laid out retirement plans and reduce purchasing power over the long haul. The key is to focus less on static fixed-income investments and more on portfolio positions that can boost your income each year. With that, investors can fight back against inflation.

Use the Dividend Screener to find the security that meet your investment criteria.