Most Americans are behind the curve when it comes to retirement savings. According to Anytime Estimate, Baby Boomers have an average of just $112,000 in retirement savings, while one in three aren’t saving anything at all. Unfortunately, the recent stock market rout erased about $3 trillion in retirement savings, setting savers back even further.

Let’s look at how non-savers can catch up, why existing investors should stay the course, and some tips to keep in mind.

To learn more about retirement topics, visit our Retirement Channel.

Lower Your Cost Basis

A non-saver investing in today’s market will have the same cost basis as someone invested in December 2020. If that market falls further, new savers could have an even lower cost basis, helping them catch up contributions by more than a year. The lower cost basis could also help them grow their portfolio faster if the market rebounds.

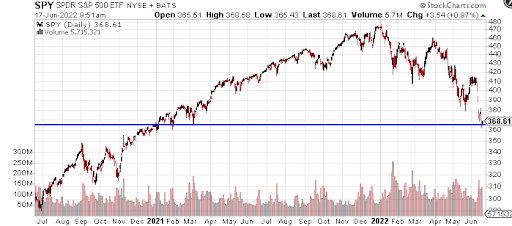

Today’s market is back down to December 2020 levels. Source: StockCharts.com

At the same time, research has made it clear that market timing is a bad idea. In other words, you should avoid waiting for the market to bottom-out before making new retirement contributions. That’s because if you had missed just five of the best days per year over the past 20 years, you’d have a 44% lower return than buying and holding!

Those already saving for retirement – but behind the curve – should also keep investing to benefit from dollar-cost averaging. By buying stocks at lower valuations, you lower your overall cost basis and create an opportunity for more significant future gains. In other words, you buy at the market tops and bottoms to even out returns.

Check out our Portfolio Management Channel to learn more about managing your portfolio.

5 Ways to Close the Gap

A market downturn may be an excellent time to catch up on retirement savings, but you need a well thought-out plan. For example, you should know how much you need to save each month to reach your retirement goals and the best places to invest to maximize your returns. Fortunately, some simple ground rules can help you succeed.

Here are a few tips to keep in mind:

- Max Out Your 401(k) First – Employer 401(k) plans have higher contribution limits than IRAs, and many employers match a certain percentage of your salary. These matches are “free” money that boosts returns beyond what the market offers.

- Save 10% for Retirement – Most experts recommend saving at least ten percent of your earnings over 40 years to maintain the same standard of living in retirement. However, financial advisors or robo-advisors can help you determine a specific number.

- Right-Size Your Risk – Increasing risk can help boost returns, but you should ensure that your portfolio remains within your risk tolerance threshold. In general, younger investors can afford to take more significant risks given their long time horizons.

- Put Savings on Autopilot – The best way to stick with your retirement savings plan is to automate withdrawals from your bank account or your employee paycheck.

- Consider I-Bonds – Series I Savings Bonds provide a nearly 10% annual yield given the high level of inflation, making them an attractive risk-free option. These bonds may be especially compelling for investors nearing or in retirement.

The Bottom Line

Bear markets may be painful for investors, but they offer an opportunity to catch up on retirement contributions and lower the cost basis of your portfolio. So if you’re behind on retirement savings, it’s an excellent time to come up with a plan to get back on track and take advantage of the current discount in the market to amplify your future returns.

Don’t forget to explore our recently launched model portfolios here.